In 2014 new legislation came into force that dictated how Capital Allowances should be treated at the point of disposal or acquisition of a commercial property owned by a UK taxpayer.

These New Rules continue to be very misunderstood and the consequences underestimated. We see more and more examples where a property transaction has taken place and the new rules have not been implemented correctly, if at all, and the net result is taxpayers are losing a benefit that they should have been entitled to. In addition to this, property advisers are exposed to negligence claims.

- Are you in the process of buying/selling a commercial property?

- Have you bought a commercial property prior to April 2014?

- Have you bought or sold a commercial property since April 2014?

- Have you completed significant property improvements to a commercial property you own or lease?

If the answer to any of these questions is yes, please call and let our expertise clarify the situation.

Case History – what can be lost?

One of our clients lost in excess of £160,000 in a transaction which was over two years old and could not be repaired and all parties thought they had implemented the new rules correctly.

Could this be you?

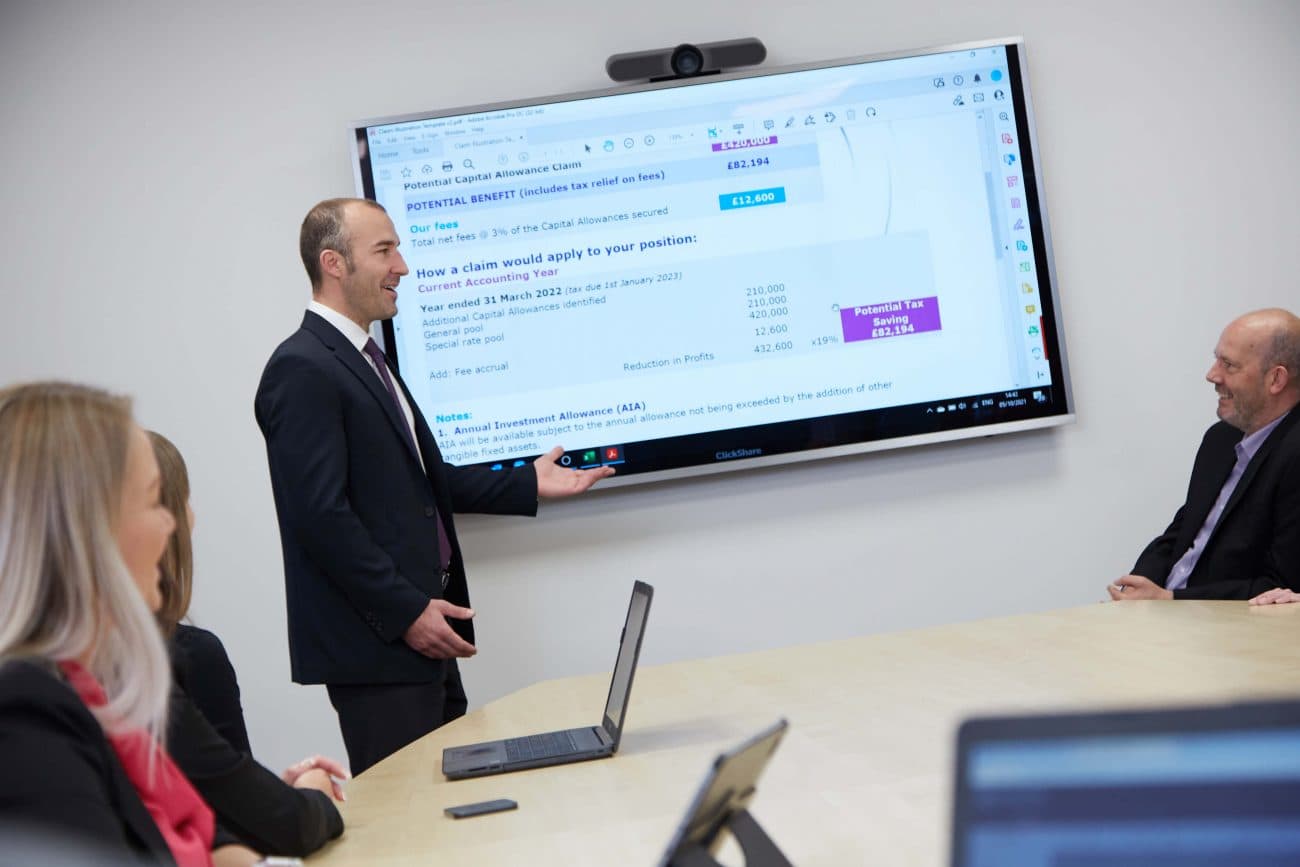

Case History – what can be gained?

When legislation is understood and applied properly, significant tax savings can be secured. The case study attached illustrates a transaction where both the Vendor and Purchaser have secured tax savings and the property advisers involved are not exposed to the risks.

If you have bought or sold a property within the last two years or in the process, contact us as we provide free support.

Latest News

26 May 2026

26 May 2026The Collaboration Between Accountants, Surveyors, and Tax Specialists in Property Claims

Capital allowance claims can unlock significant tax relief for businesses that own or invest in commercial property. Yet, despite their value, these claims are often underutilised or incorrectly prepared due to their complexity. At the heart of the process lies a combination of disciplines, tax legislation,... 21 May 2026

21 May 2026Buying a Vacant Commercial Property? Why It Could Hold Significant Tax Relief

Buying a vacant commercial property often raises concerns about repairs, tenants, and how long the building has been empty. What many buyers overlook, however, is that vacant buildings can also hold significant hidden tax relief. Even when a property is empty, valuable fixtures such as heating systems,...

Contact Us

Our expert team are here to help answer any of your capital allowances questions or enquires you have about your commercial property.